January 2026 Monthly Developer Sales Report: Primary Market Hits the Ground Running Following First CCR, OCR, and EC Launches of 2026

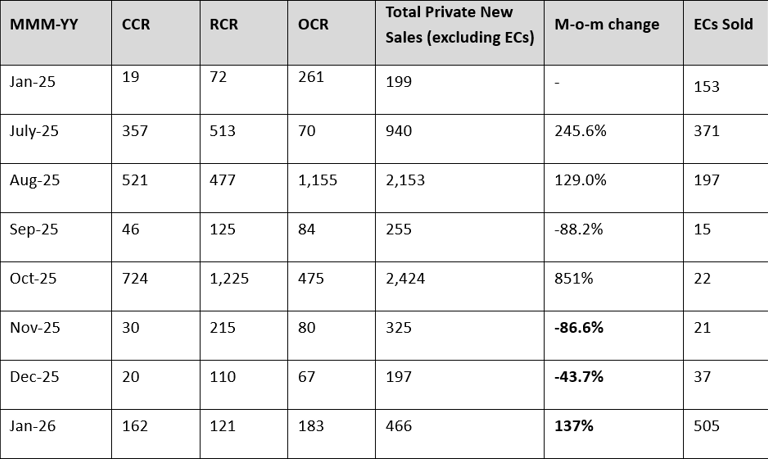

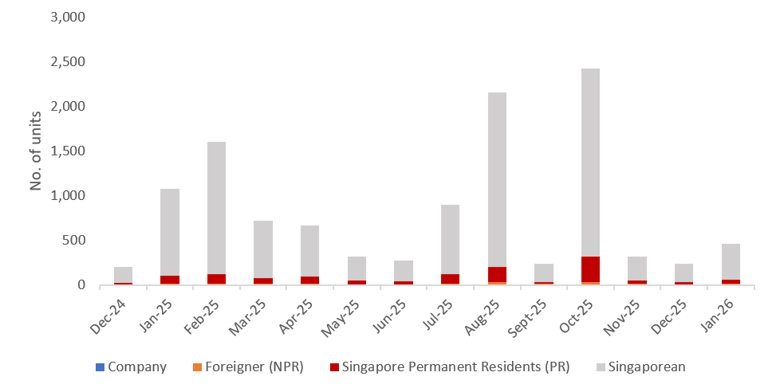

January 2026’s monthly developer sales report recorded 466 new private homes (excluding ECs), reflecting a 137% month-on-month (m-o-m) increase in transaction volume.

The rapid take-off of 2026’s new sales market was largely due to the launch of two new private home launches (Newport Residences and Narra Residences), as well as an Executive Condominium (EC) launch (Coastal Cabana). Respectively, these were the first CCR, OCR, and EC launches in the market this year.

The strong performance seen in January starkly contrasts December’s primary market, which experienced a seasonal lull with no new projects launched.

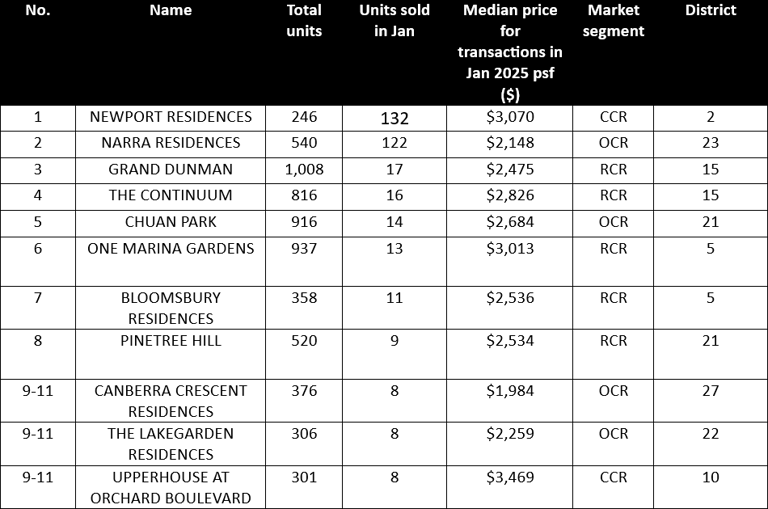

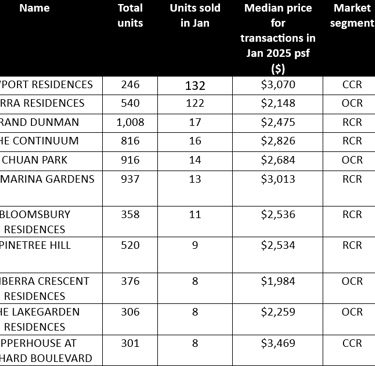

The top-selling projects for the month were the newly launched Newport Residences (132) and Narra Residences (122).

Similarly, the newly launched Coastal Cabana EC sold a whopping 505 units (67.5% of its total), making up the bulk of the 542 EC new-sale transactions in the month.

Following EC sales this month, Coastal Cabana remains the only EC project with available stock. Homebuyers and upgraders seeking an EC unit in the short term are currently limited to options in the East region, between Coastal Cabana and the upcoming Rivelle Tampines.

Table 1: New home sales over the last six months

Source: URA as at 16 Feb 2026, ERA Research and Market Intelligence

The Newport Residences Introduces New Freehold Stock into CBD

Newport Residences is located in the Central Business District (CBD) in District 2 and sold 132 (or 53.7%) of its 246 total units in January. Despite new projects in the CBD typically taking time to gain traction, Newport Residences sold over half of its units within a day.

This can largely be attributed to its competitive pricing and freehold tenure: with a median purchase price of $3,070 psf, the project offered buyers the opportunity to purchase a freehold property at just under the Core Central Region (CCR) median price of $3,072 psf in January.

The project features strong connectivity to a trio of MRT stations, being within walking distance of Tanjong Pagar MRT station on the East West Line, and the future Prince Edward Road MRT and Cantonment MRT stations on the Circle Line. The accessibility provided by a cluster of nearby MRT stations, grants residents easy access to work nodes not only in the CBD, but also at Buona Vista and One North.

However, the competitive price point, freehold tenure, CBD convenience, and proximity to Newport Plaza (the mixed-use commercial component of the residential development) made Newport Residences one of the most successful new launches in the CBD in recent years.

Narra Residences Draws in a Steady Crowd of West-Region Homebuyers

Narra Residences was the other private new home launch in January, located in the Outside Central Region (OCR) at Dairy Farm (District 23). Offering a product markedly different from Newport Residences, Narra Residences offers homebuying opportunities for HDB upgraders from Choa Chu Kang, Bukit Panjang, and Bukit Batok, as well as for right-sizers from the Hillview and Cashew landed estates.

The 540-unit project sold 122 units in January, representing about 22.6% of its total stock. The project transacted at a median price of $2,148 psf, setting a benchmark for District 23, which, as of 13th February 2026, has no new stock except the newly launched Narra Residences and 38 remaining units at The Myst (launched in 2023).

The more modest take-up rate could be due to consumer fatigue, as this is the 5th project launched in D23 (excluding ECs) since 2023.

Buyers of Narra Residences were primarily HDB upgraders looking to move into a private home in the West region amid a barren market, with no confirmed new launches aside from two upcoming EC projects at Lakeside Drive and Senja Close, which are expected to launch later in 2026. Aside from these, there are no West region GLS sites on the 1H2026 GLS confirmed list.

Coastal Cabana Sells Over a Third of its Units Like a Breeze

January also saw the first EC launch of 2026, Coastal Cabana – located in District 17. ECs in the East region of Singapore experience high demand at launch, with the most recent, Aurelle at Tampines (launched in March 2025), selling 90% of its units on launch day. Coastal Cabana sang a similar tune, selling 505 units (68%) of its 748 on launch day.

Coastal Cabana’s location is supported by the future Cross Island Line and is within a 1km priority enrolment radius of Pasir Ris Primary School and Casuarina Primary School. With these key considerations in place, the project appeals to aspiring HDB upgraders in Tampines and Pasir Ris.

Despite its strong performance, Coastal Cabana’s take-up rate may have been slightly moderated by the upcoming launch of Rivelle Tampines, located in the mature estate of Tampines and supported by an MRT station and amenities in a nearby integrated development. Given their similar location in the East, interested buyers of Coastal Cabana may be waiting for the launch of Rivelle before making an informed decision on which home best suits them.

Following EC sales this month, Coastal Cabana remains the only EC project with available stock. Homebuyers and upgraders seeking an EC unit in the short term are currently limited to options in the East region, between Coastal Cabana and the upcoming Rivelle Tampines.

Table 2: Top-performing new non-landed projects (excluding ECs) in January

Source: URA and ERApro as of 13 Feb 2026, ERA Research and Market Intelligence

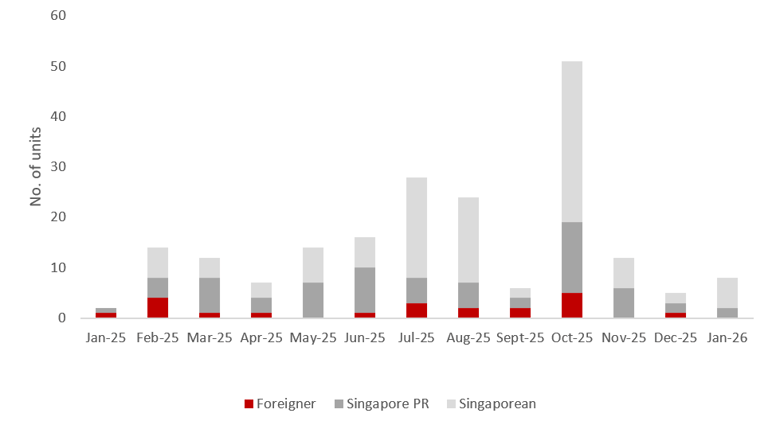

Buyer Profile

Chart 1: Buyer profile for all new non-landed homes (excluding EC)

Source: URA as at 13 Feb 2026, ERA Research and Market Intelligence

With the steep Additional Buyer’s Stamp Duty still in place, demand from foreign buyers for new private homes remained subdued. In January, foreign buyers completed only nine non-landed private home transactions (excluding ECs), accounting for a meagre 1.9% of the month’s total deals. Meanwhile, Singapore Permanent Resident buyers purchased 51 new non-landed private homes, accounting for 11.0% of all new private home (excluding ECs) purchases in the month.

Lastly, Singaporeans continued to dominate the market in January, accounting for 87.0% of new private home sales (excluding ECs), or 402 units.

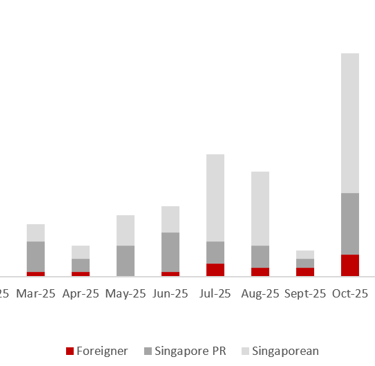

Luxury Homes

Chart 2: Buyer profile for homes transacted at $5mil and more

Source: URA as at 13 Feb 2026, ERA Research and Market Intelligence

Luxury home transactions picked up in January, with eight new non-landed private homes (excluding ECs) transacting at $5 million or more. Of these, none were by foreigners, while Singapore Permanent Residents (SPRs) and locals accounted for two and six transactions, respectively.

The highest-value transaction was a 4-bedroom premium unit (2,067 sq ft) at Newport Residences, purchased by a Singapore Permanent Resident (SPR) for $8.65 million.

Located on the former Fuji Xerox Towers site on Anson Road, Newport Residences is District 2’s newest ultra-luxury development and the Core Central Region’s (CCR) first launch of the year. Its rare freehold tenure within the Central Business District (CBD), coupled with expansive floor plates, makes it a prime choice for owner-occupiers and investors focused on legacy planning.

All other luxury transactions fell within the $5 million to $6 million range. Notably, five of these involved 5-bedroom units at Grand Dunman. This 1,008-unit mega-development in District 15 (RCR) benefits from excellent connectivity and proximity to sought-after amenities, including the Dakota MRT station and Kong Hwa School.

Closing Thoughts and Forecast

All in all, January delivered an impressive performance in the new sales market, headlined by launches across the CCR, OCR, and EC segments.

2025 was a strong year for Singapore’s private residential market, underpinned by resilient demand, steady economic conditions and renewed confidence as global risks eased. With the wind in its sails, the market is currently riding a wave of momentum, supported by attractive new launches.

In 2026, the private residential market is expected to remain resilient, with moderate price growth supported by strong owner-occupier demand and ongoing right-sizing trends. Buyers can look forward to a pipeline of 19 private residential projects, and 5 EC launches this year.

While this is lower than 2025, which saw 24 private developments and 2 EC launches, overall homebuying demand is expected to remain healthy. Barring any unforeseen circumstances, ERA Singapore projects new home sales to be between 9,000 and 10,000 units.

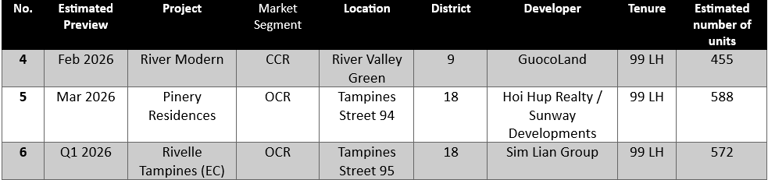

Table 3: Upcoming launches in 2025/1Q 2026

Source: ERA Project Marketing

Get in touch

Address

3721 Single Street

Quincy, MA 02169

Contacts

123-456-7890

info@email.com